Intestate Succession under the Succession Law Reform Act

When a person dies without a valid Will in Ontario, they are considered to have died “intestate”. In such situations, the distribution of their estate is governed by Part II of the Succession Law Reform Act (“SLRA”), which outlines the rules for intestate succession. The SLRA provides a default framework to determine how the deceased person’s assets will be allocated amongst their surviving family members where no valid testamentary instructions are available. The SLRA attempts to ensure the fair and equitable distribution of an intestate’s estate by creating a distribution hierarchy. Under this hierarchy, the surviving married spouse is the first to inherit, followed by the deceased’s surviving children. Ontario’s intestate succession distribution hierarchy strives to encapsulate every family scenario. Unfortunately, however, the default scheme is not perfect and often fails to accurately reflect the intestate’s wishes and intentions.

This article will explore intestate estate administration in accordance with the SLRA, applying for Certificate of Appointment of Estate Trustee without a Will (colloquially known as “Probate”), the role and responsibilities of the Estate Trustee, and the importance of having a clearly written Will to reflect your interests and intentions.

Definition of “Spouse” under the SLRA: Married vs. Common-Law

It is important to note that under section 1 of the SLRA and Family Law Act, a “spouse” means either of two persons who, (a) are married to each other, or (b) have together entered into a marriage that is voidable or void, in good faith on the part of a person relying on this clause to assert any right.[1] As such, the default entitlement granted to the surviving spouse under Part II of the SLRA specifically applies to legally married spouses. A common-law spouse is not entitled to the relief granted under this Part of the legislation.

Legally married surviving spouses are entitled to a “spousal election”. Under the Family Law Act, a legally married spouse has the option to either accept their entitlement under Part III of the SLRA or claim an equalization payment under section 6 of the Family Law Act. The election is to be made within six months of the date of death of the intestate.

Furthermore, Bill 245 — Accelerating Access to Justice Act, 2021, which came into force on January 1, 2022, introduced various revisions to the SLRA, including the non-application of the default intestacy rules to separated spouses. Under section 43.1(2) of the SLRA, a spouse is considered to be separated from the deceased person at the time of the person’s death for the purposes of subsection (1), if,

- Before the person’s death,

- They lived separate and apart as a result of the breakdown of their marriage for a period of three years, if the period immediately preceded the death,

- They entered into an agreement that is a valid separation agreement under Part IV of the Family Law Act,

- A court made an order with respect to their rights and obligations in the settlement of their affairs arising from the breakdown of their marriage, or

- A family arbitration award was made under the Arbitration Act, 1991 with respect to their rights and obligations in the settlement of their affairs arising from the breakdown of their marriage; and

- At the time of the person’s death, they were living separate and apart as a result of the breakdown of their marriage. 2021, c. 4, Sched. 9, s. 6.

As a result, separated spouses who meet the above requirements will no longer be automatically entitled to the intestate’s assets under Ontario’s intestate succession laws.

Although common-law spouses are not entitled to automatically inherit pursuant to Part III of the SLRA, a surviving common-law spouse may instead bring a claim for dependent support against the intestate’s Estate under Part V of the SLRA. Part V “Support of Dependants” mirrors Part III “Support Obligations” of the Family Law Act, which includes either of two persons who are not married to each other and have cohabited, (a) continuously for a period of not less than three years, or (b) in a relationship of some permanence, if they are the parents of a child as set out in section 4 of the Children’s Law Reform Act.[2]

Note: Claims for dependant support under Part V of the SLRA are also available to surviving spouses, married or common-law, where the deceased died with a valid Will, but failed to make adequate provisions for the proper support of his or her dependants. Under Part V of the legislation, “Dependant” means, (a) the spouse of the deceased, (b) a parent of the deceased, (c) a child of the deceased, or (d) a brother or sister of the deceased, to whom the deceased was providing support or was under a legal obligation to provide support immediately before his or her death.[3]

Further, a common-law spouse also has a priority right to act as Estate Trustee. However, if said spouse wishes to exercise that right, they would not be in a position to advance any dependency claims due to the conflict of interest in acting for and in opposition to the Estate.

Intestate Estate Administration Under the SLRA

Note: For the purposes of this section, the term “spouse” refers specifically to a legally married individual per section 1 and Part III of the SLRA.

Scenario One – Spouse and No Children (s. 44)

If the deceased person leaves a spouse, but no children, the surviving spouse will receive the entire estate.

Scenario Two – Spouse and One Child (s. 46(1))

If the deceased person leaves a spouse and one child, the surviving spouse will receive the first $350,000.00 (“preferential share”), and the remainder will be divided equally between the spouse and the child. Note: For individuals who have died before March 1, 2021, the amount of the surviving spouse’s preferential share remains $200,000.00.

Scenario Three – Spouse and Children (s. 46(2))

If the deceased person leaves a spouse and children, the surviving spouse will receive the first $350,000.00 (“preferential share”) and one-third of the residue of the estate, the remainder of the assets are then divided equally among the children. Furthermore, where a person dies intestate in respect of property having a net value of not more than the preferential share ($350,000) and is survived by a spouse and children, the spouse is entitled to the property absolutely (s. 45(1)).

Scenario Four – No Spouse and Children (s. 47(1) and (2))

If the deceased person does not have a spouse but has children, the children will each inherit an equal portion of the estate. If any of the children are predeceased, that child’s descendants will inherit their specific share.

Scenario Five – No Spouse and No Children (s. 47(3))

If the deceased person does not have a spouse or children, the estate will be split equally between the Deceased’s parents. If there is only one surviving parent, then they will inherit the entirety of the estate.

Scenario Six – No Spouse, No Children, and No Parents (s. 47(4))

If the deceased person does not have a spouse, children, or surviving parents, the estate will be distributed among surviving siblings of the Deceased in equal shares. If any of the siblings predeceased the intestate, their share of the estate will be distributed among their children equally.

Scenario Seven – No Spouse, No Children, No Parents, and No Siblings (s. 47(5))

If the deceased person does not have a spouse, children, surviving parents, or siblings, the estate shall be distributed equally amongst the nieces and nephews of the deceased.

Scenario Eight – No Spouse, No Children, No Parents, No Siblings, and No Nieces/Nephews (s. 47(6) and (7)

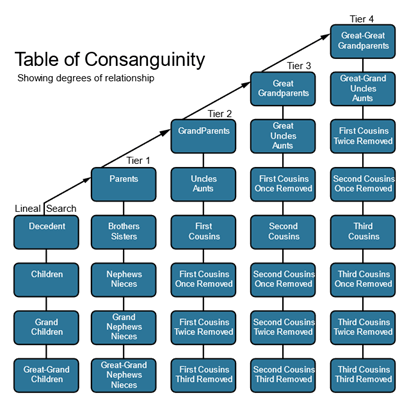

If the deceased person does not have a spouse, children, surviving parents, siblings, or nieces/nephews, the estate shall be distributed among the closest next of kin. If there is no discernible next of kin, the property of the intestate becomes the property of the Crown, and the Escheats Act, 2015 applies.

For the purposes of this section of the legislation, the “closest next of kin” is the closest blood relative to the deceased and is determined by “counting upward from the deceased to the nearest common ancestor and then downward to the relative.”[4] See the attached Table of Consanguinity.

Application for Certificate of Appointment of Estate Trustee Without a Will

The first step in administering the estate of an intestate individual is the appointment of an Estate Trustee. If no Will exists to name an executor or if that portion of the Will is deemed to be invalid, an individual must apply for a Certificate of Appointment of Estate Trustee Without a Will. This Certificate formally appoints the Estate Trustee by the Superior Court of Justice in the jurisdiction in which the party deceased, who will then be responsible for managing and distributing the Deceased’s estate.

Steps in the Application Process:

- Who Can Apply?

Anyone resident in the Province of Ontario who is of the age of majority can apply to become the Estate Trustee where there is no Will. However, there is a priority selection found in the SLRA that provides for the order of appointment. Priority will be given to the surviving spouse of the deceased, then to the deceased’s closest living relative. As previously mentioned, common-law spouses are included in this definition of “spouse” for the purposes of priority selection in applications for Appointment. Where the person highest in order of entitlement applies, there is no need to obtain renunciations or consents from the other candidates. However, if the applicant is not the highest in the order of priority, then they will be required to provide renunciations from anyone with a stronger priority claim. Failure to provide these renunciations will result in the need for further judicial intervention. - Documents Required: The applicant must provide various documents, including:

- The deceased’s death certificate;

- Proof of their relationship to the deceased (e.g., marriage certificate, birth certificate);

- Necessary application forms, including the Application (Form 74A), Affidavit of Service (Form 74B), Affidavits (as required), and Death Certificate of Appointment of Estate Trustee (Form 74C).

- Filing with the Court: The application is filed with the Ontario Superior Court of Justice. If there are no disputes, the court typically grants the certificate, enabling the Estate Trustee to begin the probate process and manage the estate. The Estate Trustee must pay Estate Administration Tax when you submit your application with the court. Estate Administration Taxes are owed on Estates with a value of more than $50,000.00 and are 1.5% of the value of the Estate over this amount.

Responsibilities of the Estate Trustee

Once appointed, the Estate Trustee has several critical duties and responsibilities, including:

- Gathering and managing assets: The Estate Trustee must identify and take possession of the deceased’s assets, including real estate, bank accounts, investments, and personal property. The Estate Trustee has a duty to safeguard and preserve the assets of the estate.

- Paying debts and taxes: The estate trustee is responsible for paying any debts owed by the estate, including taxes, funeral expenses, and other liabilities.

- Distributing the estate: After all debts and taxes are settled, the Estate Trustee will distribute the remaining assets according to the rules of intestate succession outlined in the SLRA.

- Keeping records: Estate Trustees must keep and maintain a detailed accounting of all financial transactions related to the estate, including receipts, disbursements, and taxes paid.

In cases where the Estate Trustee is not fulfilling their responsibilities or is acting improperly, an interested party (such as a beneficiary or creditor) can apply to the court for removal of the Trustee. It is important to note the Estate Trustees have assumed considerable personal liability. If the Estate Trustee fails to maintain adequate records or there are withdrawals of Estate funds unsupported by invoices or receipts, the beneficiaries of the Estate may have a valid claim against the Trustee personally, despite there being no ill intent on the part of the Estate Trustee. Furthermore, Estate Trustees must obtain a clearance certificate form the Canada Revenue Agency (CRA) before distributing any property under his or her control. The certificate guarantees that any taxes, penalties, or interest payable by the Estate have already been paid prior to distribution of the Estate. Pursuant to the Income Tax Act, failure to obtain a clearance certificate renders the Estate Trustee personally liable for any unpaid taxes, interest, or penalties of the Estate to the extent of the value of the property distributed to the beneficiaries.[5]

The Importance of Having a Will

While intestate succession under the SLRA provides for a default framework for the distribution of an estate, they may not reflect the wishes or intentions of the deceased. As discussed, the default framework does not provide any entitlement for common-law spouses to inherit under the SLRA. A valid Will gives you the opportunity to name your preferred Estate Trustee, minimize family disputes, plan for your dependents, incorporate tax-planning strategies, and distribute your life’s earnings in accordance with your wishes. This is why it is critically important to have a clearly written Will.

At Northern Law LLP, we have lawyers ready to assist and help guide you through the process of planning for your future and ensure that your wishes are respected. If you have questions regarding Will drafting, estate planning, or are looking to discuss the particulars of your situation, contact us at (705) 222-0111 or info@northernlaw.ca.

[1] Succession Law Reform Act, R.S.O. 1990, c. S.26, s. 1; Family Law Act, R.S.O. 1990, c. F.3, s. 29, s. 1.

[2]Family Law Act, R.S.O. 1990, c. F.3, s. 29.

[3] Succession Law Reform Act, R.S.O. 1990, c. S. 26, s. 57.

[4] Succession Law Reform Act, R.S.O. 1990, c. S. 26, s. 47(8).

[5] Income Tax Act, R.S.C., 1985, c. 1 (5th Supp.), s. 159(3).